Blog

Keep up to date with our news, tips & tricks, and latest information!

Asset Protection 101: A Guide for Women Entrepreneurs

Jeff Martin, CRPC®, Financial Advisor in Arizona

The fourth quarter of the year is crucial as it represents an opportunity to assess the past year's portfolio performance, gauge current investment strategies, and lay the groundwork for the coming year. These end-of-year reviews are more than just reviewing the highs and lows of market performance. Instead, they provide thoughtful insights that can impact the financial strategies used as one works toward their goals in the forthcoming year.

Here are the five critical areas that a fourth-quarter review will assess.

Portfolio performance

Fourth-quarter reviews enable investors to measure how well their portfolio has performed against projected outcomes and predefined goals. This assessment helps investors and financial professionals evaluate the...

more

4th Quarter Financial Reviews: 5 Critical Areas to Assess

Jeff Martin, CRPC®, Financial Advisor in Arizona

The fourth quarter of the year is crucial as it represents an opportunity to assess the past year's portfolio performance, gauge current investment strategies, and lay the groundwork for the coming year. These end-of-year reviews are more than just reviewing the highs and lows of market performance. Instead, they provide thoughtful insights that can impact the financial strategies used as one works toward their goals in the forthcoming year.

Here are the five critical areas that a fourth-quarter review will assess.

Portfolio performance

Fourth-quarter reviews enable investors to measure how well their portfolio has performed against projected outcomes and predefined goals. This assessment helps investors and financial professionals evaluate the...

more

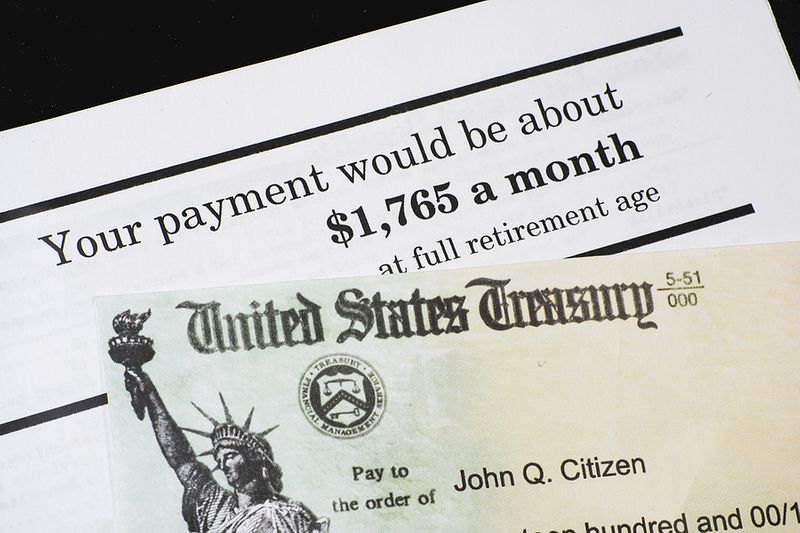

Social Security Retirement: Proposed Changes for 2025

Jeff Martin, CRPC®, Financial Advisor in Arizona

As the U.S. population ages and life expectancies continue to increase, Social Security policymakers and experts are considering various adjustments and updates to the program to help lengthen its long-term sustainability. Three significant discussions are underway that may impact Social Security retirement benefits starting in 2025.

Using a different index to determine COLA

Another proposed change concerns calculating cost-of-living adjustments (COLA) for Social Security retirement benefits. Some policymakers have suggested using a different index, such as the Chained Consumer Price Index for All Urban Consumers (C-CPI-U), to accurately reflect changes in the cost of living. This adjustment could result in a lower annual increase in benefits but may help...

more

An 8-Step Approach for Impactful Giving

Jeff Martin, CRPC®, Financial Advisor in Arizona

Many individuals' wealth comes with the ability to create thoughtful and impactful change for others. However, making the foundation for impactful giving requires strategic planning and understanding how to transform their assets into lasting legacies. With a comprehensive approach, giving-minded individuals can skillfully transfer their assets into an enduring legacy that impacts communities and causes they care about.

This outlines how individuals can use an eight-step approach to engage in thoughtful and impactful giving that transforms assets into positive change.

Begin with a Strategic Giving Plan

The path from assets to impactful legacies must always start with a strategic giving plan. Strategic planning aligns your...

more

5 Reasons Financial Professionals Discuss Insurance with Clients

Jeff Martin, CRPC®, Financial Advisor in Arizona

Financial professionals often discuss insurance with their clients because it is an essential component of comprehensive planning. While many people associate financial professionals solely with investments and planning for retirement, the reality is that insurance plays a crucial role in protecting and preserving wealth.

This article discusses the five reasons financial professionals discuss insurance with their clients during meetings and suggests specific insurance products.

Risk mitigation

One of the primary reasons financial professionals discuss insurance with their clients is to mitigate risk. Insurance products such as life insurance, disability insurance, and long-term care insurance can help safeguard against unexpected events that could...

more

Transforming From a Spender to a Saver: A Personal Journey to Financial Independence

Jeff Martin, CRPC®, Financial Advisor in Arizona

Are you tired of living paycheck to paycheck, feeling like you never have enough money to cover your expenses and save for the future? If so, you're not alone. Many people struggle with transitioning from being a spender to a saver. However, with the right mindset and some strategic changes, you can transform your financial habits and start building a more secure future for yourself. Here are the steps to take toward this transformation.

Assess Your Current Situation

The first step in transforming from a spender to a saver is to examine your current financial situation carefully. This examination includes understanding your income, expenses, and debt by outlining your monthly payments, including bills, groceries, entertainment, and other discretionary...

more

A Long-term Care Guide for Singles

Jeff Martin, CRPC®, Financial Advisor in Arizona

Understanding what long-term care (LTC) entails is vital in formulating an appropriate care plan. LTC refers to services designed to help care for an individual's health or personal care needs for a short or extended period. These services assist people in living independently and safely when they can no longer perform everyday activities independently.

But for single individuals, the need for LTC services might be more imminent due to a lack of partner or immediate family support. Planning for long-term care (LTC) is essential to financial management and personal well-being.

Addressing this crucial need has become more pertinent with the ever-increasing healthcare costs and a growing aging population. This articles addresses the six steps singles must comprehensively...

more

A Recap of 2024 Retirement Savings Legislation

Jeff Martin, CRPC®, Financial Advisor in Arizona

The landscape of retirement savings in the United States is experiencing crucial changes following newly enacted legislative changes for 2024. These updates and reforms seek to enhance the flexibility of retirement savings accounts and transform how Americans save and prepare for retirement. Here are some of the more significant changes this year.

Contribution increase

One key 2024 retirement savings legislative update pertains to contributions into retirement plans such as the 401(k). The legislation introduces a significant increment in contribution limits, allowing Americans to save more for retirement. This change enables individuals to accumulate a more substantial retirement savings nest egg and allows them to manage their taxable income, given the...

more

Investing Wisely in Your Golden Years: A Guide for Arizona Retirees

Jeff Martin, CRPC®, Financial Advisor in Arizona

Retirement is a time to enjoy the fruits of your labor. But even after you have stopped working, it's important to make sure your money continues to work for you. Investing wisely can help you maintain your lifestyle, protect your nest egg, and even leave a legacy for your loved ones. Here’s a straightforward five-step guide to help you navigate investing after retirement.

Step 1: Revisit Your Financial Plan

Financial planning is not just for building wealth—it’s equally important during the years you’re spending it. The economic landscape, marked by events like the pandemic and market fluctuations, can impact your retirement portfolio. It is wise to sit down with your financial advisor to review your investment portfolio. Make sure your investment...

more

7 Benefits of Inflation

Jeff Martin, CRPC®, Financial Advisor in Arizona

When inflation increases, people often feel the sting of paying more for groceries, gas, and almost everything else. Many may feel inflation is terrible because their paychecks are shrinking, and they don't like paying more for the same items. But inflation also has positive benefits that may occur over time, such as:

Wages increase- Employers often increase wages for their current employees and new hires to attract and retain workers during inflation. For a period, inflation may increase job openings at employers with lower wages until they increase their wages too. Higher wages bring more money into the economy as workers have more money to spend.

Property values increase- Pre-existing homes, automobiles, and some investment strategies...

more

How Working Teens Can Invest Early with a Roth IRA

Jeff Martin, CRPC®, Financial Advisor in Arizona

When working teens invest early in a Roth IRA, they can contribute to a strategy that could accumulate millions later in retirement. Working teens can contribute to a Roth IRA when a parent or grandparent opens the account. A Roth IRA can be opened at any age if a child has income. For example, if your five-year-old child was a model for a local store and received a paycheck in their name, the amount received can be contributed to a Roth IRA.

Working teens receiving W-2 income with a checking account in their name can have automatic contributions deducted and deposited into their Roth IRA. Or, if the teen doesn’t receive a W-2 for money from mowing lawns, babysitting, or other work, the income must be reported to the IRS through income tax filing to qualify for Roth IRA...

more

401(k) Options for Small Business Owners

Jeff Martin, CRPC®, Financial Advisor in Arizona

Regardless of the business's size, small business owners have 401(k) retirement savings plan options that may be suitable for their situation. Business owners must plan for retirement by utilizing retirement savings vehicles that may provide them with common IRS tax savings incentives when funding specific 401(k) options.

A business owner can open several retirement savings plan types if they're the only employee or have anywhere from two to 100 employees. As you work with your financial and tax professionals to determine which is appropriate for your small business, we outline what to know about each:

Solo 401(k)- A solo 401(k) is a retirement savings plan for self-employed business owners who want to maximize their retirement contributions. It's also...

more

5 Tax Breaks for College Students and Parents

Jeff Martin, CRPC®, Financial Advisor in Arizona

With the cost of college expensive for many, receiving a tax break from the IRS for college-related expenses may be appealing. 529 Plans and Coverdell Education Savings Accounts (ESAs) offer tax-advantaged withdrawals when used for qualified expenses.

But for those seeking an additional tax deduction on their tax return, there are specific tax credits that students and their parents may qualify for. However, many tax credits come with rules, so you must work with your tax and financial professional to determine which applies to your situation. Here are the tax credits you may qualify for in 2023 or the future, pending no changes in IRS education expenses deduction rules:

1. The American Opportunity Tax Credit (AOTC)- This tax credit is for single tax...

more contributions.")

Maxed Out Your 401(k)? Here's What To Do Next

Jeff Martin, CRPC®, Financial Advisor in Arizona

Investing is a complex process that requires careful thought, strategy, and an understanding of various factors that could influence your portfolio's performance. Many investors understand the significance of market trends, economic cycles, and changing consumer behavior. However, politics is another The 401(k) plan is an excellent way for working Americans to save for retirement. For many, hitting the maximum contribution limit is a goal that many work toward to reap the benefits of saving tax-deferred. But what happens when you've maxed out your 401(k) contributions and want to continue saving for an independent and comfortable retirement?

Maxing out your 401(k) is a significant achievement toward securing an independent financial future. However, several other investment...

more

Politics and Your Portfolio: Understanding the Impact on Investment Performance

Jeff Martin, CRPC®, Financial Advisor in Arizona

Investing is a complex process that requires careful thought, strategy, and an understanding of various factors that could influence your portfolio's performance. Many investors understand the significance of market trends, economic cycles, and changing consumer behavior. However, politics is another crucial aspect that often needs to get the attention it merits. The link between politics and your investments is more profound than one might initially expect.

To truly grasp how politics impacts investment performance, it's necessary to consider multiple dimensions. Elections, policy changes, geopolitical events, and even political rhetoric can influence economic activities, indirectly affecting the financial markets. Thus, as an investor, understanding the correlation between...

more

6 Things That Can Deter You From Accumulating Wealth

Jeff Martin, CRPC®, Financial Advisor in Arizona

Many people encounter many obstacles in pursuing financial independence and wealth accumulation. These obstacles may seem insignificant at first glance, but they can drastically impact one's capability to acquire wealth. Understanding what may hinder one from accumulating wealth is crucial. This article explores the obstacles that can deter you away from financial confidence and your wealth accumulation journey.

Living beyond your means

Living beyond your means is one of the primary obstacles to wealth accumulation. The pattern of overspending, whether through extravagant lifestyle choices, impulsive purchases, or excessive credit card use, can ultimately lead to excessive debt. By spending more than you earn, you're denying yourself the chance to save and...

more

How to Quickly Build a Vacation Fund

Jeff Martin, CRPC®, Financial Advisor in Arizona

Vacation should be a time of relaxation and fun. But sometimes, a vacation can follow us home in the form of debt. Preparing your finances for going on vacation and paying the expenses associated with it is essential to avoid financial stress afterward. Here are some ways to quickly build a vacation fund and save money along the way.

Establish a vacation budget- The first step is establishing a vacation budget to help you understand how much you can afford to spend. Start by assessing your current financial situation. How much extra income do you have right now that could be redirected towards your vacation? Consider any upcoming bills or other financial obligations. Once you have a rough idea of the disposable income you can use, you can begin allocating funds...

more

What is Direct Indexing, and Why Do Investors Use It?

Jeff Martin, CRPC®, Financial Advisor in Arizona

Direct indexing, also known as separate accounts or tailored portfolio management, is an investment strategy providing advanced portfolio customization and tax efficiency.

Direct indexing does not involve purchasing shares in mutual funds or exchange-traded funds (ETFs). Instead, it involves buying individual securities comprising a certain index such as the S&P 500, NASDAQ, or any other market index. Here are a few reasons an investor may use a direct indexing strategy.

Flexibility

The draw of direct indexing lies in its flexibility. An investor can adjust the portfolio holding to include or exclude certain stocks based on personal preferences, ethical concerns, or tax considerations. In contrast, traditional methods like ETFs and mutual funds...

more

Legacy Planning: An Essential Tool for Passing Wealth and Continuing Values

Jeff Martin, CRPC®, Financial Advisor in Arizona

Legacy planning involves leaving more than financial assets for future generations. It's about preserving and continuing one's values, life experiences, and personal philosophies. It is a holistic approach to managing wealth, typically involving multiple generations developing and implementing the plan.

Legacy planning covers traditional estate planning activities such as trusts and asset distribution but includes broader considerations, such as how a person wants to be remembered. Here are some of the critical actions involved in legacy planning.

Understanding assets and liabilities

The first step in legacy planning involves clearly understanding your financial assets and liabilities. This first step entails analyzing your investments, properties,...

more

Why Families Consider Long-Term Care for Loved Ones

Jeff Martin, CRPC®, Financial Advisor in Arizona

Long-term care (LTC) is an essential component of healthcare that aids individuals who are physically or mentally incapable of independent living. While it may seem daunting, LTC offers numerous benefits that can significantly enhance the quality of life and overall well-being of those in need.

Families often find themselves considering long-term care options for their loved ones due to a variety of reasons. One significant cause is the inevitable progression of age, which can bring about several health issues and an overall decline in the ability to perform daily tasks independently. Here are four reasons why families consider LTC for their loved ones.

Personalized Care

One of the most significant benefits of LTC is the provision of personalized...

more

Ways Heirs Can Prepare to Inherit

Jeff Martin, CRPC®, Financial Advisor in Arizona

Over the next few decades, an estimated $30 trillion in assets will pass to heirs. This wealth transfer provides opportunities and challenges for those who will inherit this wealth. Financial independence is paramount to understanding the implications of wealth transfer and adequately preparing for it. Here, we explore five key actions heirs must focus on as they prepare to inherit.

Open communication

Engaging in open and honest conversations about wealth transfer with the generation passing on the wealth is essential. Although discussing inheritance matters can be uncomfortable, it ensures all parties are on the same page and enables the younger generation to appreciate the responsibilities involved. Understanding what to expect can significantly manage...

more

Variables Impacting Homebuyers This Year

Jeff Martin, CRPC®, Financial Advisor in Arizona

As we look into 2024, predicting the trajectory of mortgage interest rates has never been more critical for prospective homebuyers. Understanding the factors influencing these rates and how they may play out can help potential homeowners make informed decisions.

Several variables weigh heavily on the direction of mortgage rates, including the state of the economy, monetary policy, inflation, and housing market conditions. Unfortunately, global economics is a highly intricate system, and these factors can change unexpectedly due to unforeseen events.

However, as challenging as forecasting may be, it's crucial to the planning process for future homeowners. So, despite the unpredictability, let's delve into some insights that may continue to impact mortgage rates throughout...

more

A ‘How-To’ Guide for Building a Vacation Fund

Jeff Martin, CRPC®, Financial Advisor in Arizona

An escapade to an exotic getaway or a relaxing vacation provides an opportunity for rejuvenation. However, these leisure vacations often come with a price tag.

Establishing a vacation fund is crucial to enjoying your holiday without financial strain. Here are some practical tips to help you build your vacation fund effectively.

1. Establish a budget.

Before saving for the vacation, establish a budget to cover your daily living expenses, including groceries, bills, mortgages, and emergency funds. After covering these necessities, identify how much money you can devote to your vacation fund.

2. Set clear vacation fund goals.

Having a distinct vacation goal can inspire motivation....

more

The Numerous Benefits of Charitable Giving

Jeff Martin, CRPC®, Financial Advisor in Arizona

Charitable giving is an integral part of many individuals' financial strategy, not only as a means of helping others but also for the numerous benefits it offers to the giver. Here, we delve into ten benefits that further underscore the importance of charitable giving.

Tax deductions- One immediate benefit of charitable giving is the potential for considerable tax deductions. Assets or cash donated to non-profit organizations can generally be deducted from income tax, significantly reducing the overall tax obligation for many individuals.

Legacy building- Through substantial charitable donations, individuals have the unique opportunity to leave a lasting legacy. The ripple effect of their contributions can be sustained for generations,...

more

A 6-Step Financial Action Plan for Divorcees

Jeff Martin, CRPC®, Financial Advisor in Arizona

Going through a divorce can be an emotionally charged and stressful event. Aside from the emotional toll, there's often the challenging task of disentangling finances and assets, a process that frequently leaves many divorcees in a precarious financial situation. However, it is essential to remember that this is not the end of the road—with a comprehensive strategy, you can rebuild your finances post-divorce. Here is a guide for divorcees seeking a fresh start for their finances.

1. Cut down on unnecessary spending.

Divorce usually means moving from a dual-income lifestyle to a single-income household. Therefore, some lifestyle adjustments may be necessary, at least temporarily. Review your recurring expenses and identify areas where you...

more

IRS 2025 Revenue Proposals: Potential Impacts to Estate Planning?

Jeff Martin, CRPC®, Financial Advisor in Arizona

The Internal Revenue Service (IRS) has proposed several significant changes to the tax code as part of its revenue proposals for 2025. If enacted, these changes could have profound implications for estate planning.

As estate law and financial professionals closely monitor these potential revisions, it's crucial for individuals interested in safeguarding their wealth for future generations to stay informed about these impending changes.

The IRS's 2025 revenue proposals target wealthy individuals, potentially impacting estate planning strategies. These proposals include raising the top income tax rate, taxing capital gains at death, eliminating the stepped-up basis for capital gains, limiting the annual gift exclusion, reducing the estate and gift tax exemption amount, and...

more

The Seven Economic Indicators Investors Must Monitor

Jeff Martin, CRPC®, Financial Advisor in Arizona

Understanding the many economic indicators that can impact your portfolio's performance is essential as an investor. Monitoring these indicators can help you better predict patterns, identify trends, and make informed investment decisions.

Here are some key economic indicators to watch this year.

Gross Domestic Product (GDP) — measures a country's total economic output over a specified period. It essentially represents an economy's size and growth rate, making it a fundamental indicator for investors to monitor. A growing GDP signifies a healthy economy, often leading to stronger corporate profits and higher stock prices.

Unemployment Rate—The unemployment rate is another critical indicator of an economy's health. High unemployment...

more

Tips to Help You Spring Clean Your Financial Life

Jeff Martin, CRPC®, Financial Advisor in Arizona

Spring is a great time to declutter your homes and an excellent opportunity to clean up your financial life. Spring cleaning must involve reviewing, reorganizing, and eliminating unnecessary financial clutter to help make your money management more efficient.

Despite the significance of spring cleaning, financial cleaning is an area that tends to be overlooked during the spring cleaning spree. To start spring cleaning your finances, you must separate your financial life into critical sections, highlighted in the seven steps below.

Step #1— Analyze your budget. Compare your current expenditures with your income streams. Examine your bank statements, credit card invoices, and receipts to assess where your money is going. This review will help provide insight...

more

4 Trends Set to Impact Earnings Season 2024 and Beyond

Jeff Martin, CRPC®, Financial Advisor in Arizona

The financial ecosystem is ever-evolving, and the 2024 earnings season is no exception. Consistently, each earnings period generates a flurry of activity among investors across the globe as publicly traded companies release their quarterly or annual earnings reports.

For investors, this event indicates stock market performance and dictates subsequent strategic portfolio decisions.

We have observed significant transformations in the earnings season due to many factors. Technological advancements, other dynamics such as global economic conditions, and regulatory changes reshape earnings seasons in ways we haven't seen before. Here are the trends set to impact earnings season this year and beyond

Digitization

With the continued adoption of powerful...

more

Ways Women Investors Differ from Men Investors

Jeff Martin, CRPC®, Financial Advisor in Arizona

In the world of finance and investing, it is no secret that the majority of investors are men. However, with an increasing number of women investing independently, it is essential to understand how women investors differ from their male counterparts. While both men and women share the same goal of growing wealth, their approaches, preferences, and concerns can vary significantly. Here are some key aspects to consider when examining the differences between men and women investors.

Risk tolerance

One of the most significant differences between men and women investors is their risk tolerance. Studies have shown that women are more risk-averse than men regarding investing, which could be due to various factors, such as cultural and societal...

more

Tips to Help Investors Ignore ‘News Noise’

Jeff Martin, CRPC®, Financial Advisor in Arizona

In today's fast-paced world, it's all too easy to get caught up in the constant flow of news and information. As investors, it's crucial to stay informed about the market and economic trends. Equally vital is the ability to filter out the noise that isn’t relevant. Here are four essential tips to help investors ignore the ‘news noise’ and stay laser-focused on their goals.

Tip #1- Distinguish between noise and relevant information.

Firstly, it's important to distinguish between noise and relevant information. Noise refers to the constant buzz of sensational headlines and short-term market fluctuations that have little impact on long-term investment strategies. On the other hand, relevant information includes data, research, and analysis that provide...

more

A Focus on Sustainable and Ethical Investing

Jeff Martin, CRPC®, Financial Advisor in Arizona

Sustainable and ethical investing, or socially responsible investing (SRI), refers to investing in companies that prioritize environmental, social, and governance (ESG) factors in their operations. SRI goes beyond financial returns and considers the impact of a company's actions on people and the planet.

There has been a significant surge in global interest in SRI in recent years. According to a Global Sustainable Investment Alliance report, the global market for SRI has now exceeded a staggering $30 trillion, a clear indication of the growing demand for socially responsible investments. This trend is driven by the increasing awareness of environmental issues and the desire to align one's values with financial goals.

One of the main principles of SRI is managing and...

more

Why Americans Should ‘Double Down’ on Reducing Debt

Jeff Martin, CRPC®, Financial Advisor in Arizona

As Americans, we often pride ourselves on our independence, self-sufficiency, and living the American Dream. However, one thing that can hold us back from truly living our full potential is debt. In recent years, the average American household has accumulated significant debt, whether credit card debt, student loans, or mortgages. Shockingly, Americans rank third in debt compared to other countries. This alarming statistic underscores the urgent need to change our mindset and 'double down' on reducing personal debt.

How debt impacts our lives

The first step toward reducing debt is understanding its impact on our lives. Debt is more than just a financial burden; it can affect our mental and emotional well-being. The constant stress and worry...

more

10 Reasons Why High-Performers Seek Financial Help

Jeff Martin, CRPC®, Financial Advisor in Arizona

Often, there is a misconception that seeking financial help indicates incompetence or lack of financial self-sufficiency. However, seeking help is the exact opposite. High-performing individuals who excel in their respective fields adopt a more pragmatic approach- they understand the importance and benefits of employing a financial professional's services.

Seeking the help of a professional to assist in one's wealth planning leaves more time for them to focus on their primary specialty area, thus driving efficiency in managing results. Often, these individuals are focused on their careers, are business owners, or are high achievers with many goals. Here are ten ways a financial professional can assist high-performing individuals work toward improving their financial...

more

How Social Security Impacts Retirement Planning

Jeff Martin, CRPC®, Financial Advisor in Arizona

As people approach their golden years, planning for retirement often becomes a focal point of their financial strategies. One aspect of planning that sometimes creates confusion or misinterpretation is the role of Social Security retirement benefits. Understanding how Social Security Retirement fits into retirement can be crucial as it may influence other planning decisions.

Social Security is a government-run program that provides financial assistance to eligible retirees through monthly payments. Contrary to popular belief, Social Security is not meant to be a primary source of retirement income but rather a safety net or supplement. Here are essential features of Social Security retirement to consider when planning for retirement.

...

more

The Future of Work: AI, Diversity and Inclusion

Jeff Martin, CRPC®, Financial Advisor in Arizona

With the rise of automation, artificial intelligence (AI), and the gig economy, the workforce is transforming significantly. As we move towards the new decade, businesses and individuals must understand the future workforce trends and prepare accordingly.

One of the most significant changes we can expect in the future workforce is the increased use of automation and AI. These technologies have steadily gained momentum and are predicted to take over many routine and repetitive tasks. AI may impact both blue-collar jobs and white-collar professions such as accounting, data entry, and law. The thought of robots taking over human jobs may seem unsettling, but it's crucial to note that this shift may also create new job opportunities in fields such as data science, programming, and...

more

Home Buying Season: 10 Tips to Help Guide the Process

Jeff Martin, CRPC®, Financial Advisor in Arizona

Spring is known as the prime season for homebuyers. The warmer weather, blooming flowers, and longer days make it the perfect time to start the search for a new home. However, with the competitive market and limited inventory, buying a home in the spring can be challenging. To help prospective buyers navigate the home-buying season, here are ten tips to guide the home-buying process.

1. Start loan pre-approval early. Spring is a popular time for homebuyers, so competition can be fierce. It's essential to start preparing early by getting pre-approved for a mortgage, organizing your finances, and creating a list of must-haves for your new home.

2. Work with a professional Real Estate agent. A professional real estate agent is your best ally...

more

Financial Independence Together: 7 Essential Actions for Couples

Jeff Martin, CRPC®, Financial Advisor in Arizona

Planning for the financial future as a couple is crucial to building a life together. Planning is vital in strengthening a relationship's bond of trust and understanding. When couples plan together, they often practice good financial management skills and communication, creating a comprehensive financial future. Here are seven essential tips to help couples work toward their goals.

Tip #1- Practice open communication.

Discussing finances might not be the most romantic topic for couples, but it is instrumental for a healthy relationship. Both partners must discuss and disclose their financial status, including debts, savings, investments, and financial habits. Open communication helps understand each partner's financial position and aids in...

more, and IRA documents with a calculator, representing retirement planning options.")

A Look into the 2024 IRS Retirement Savings Thresholds

Jeff Martin, CRPC®, Financial Advisor in Arizona

The Internal Revenue Service (IRS) plays a central role in ensuring fiscal discipline while at the same time providing a stable economic platform for long-term financial growth. One of the IRS's areas of emphasis is retirement savings, with regulations adjusted annually to cater to the changing economic landscape. This piece seeks to review the 2024 IRS retirement saving thresholds, giving readers a glimpse into the future as they plan their retirement savings.

The IRS adjusts its retirement savings thresholds, reflecting the changes in the cost of living and inflation rates. The primary reason for these changes is to encourage individuals to save for retirement and to ensure that the retirement savings system remains fair and equitable. Understanding these thresholds helps...

more

How to Prevent a Credit Crisis

Jeff Martin, CRPC®, Financial Advisor in Arizona

A personal credit crisis is something many people fear, as it can lead to financial ruin and burden an individual with immense debt. Credit issues can lead to numerous problems such as legal judgments, fraud, overspending, and negative impacts on your credit score. Fortunately, steps can be taken to avoid such a crisis. Here are eight things that can help you manage your finances and prevent a credit crisis.

1. Budget and track expenditures. It's essential to maintain a strict budget irrespective of the size of one's income. Uncontrolled spending can lead to incurring a significant amount of debt, which in turn can trigger a credit crisis. It's vital to always keep a detailed record of expenditures to prevent overspending and stay within a...

more

Why Financial Fraud is Becoming Harder to Spot: AI

Jeff Martin, CRPC®, Financial Advisor in Arizona

As we continue to navigate the digital era, Artificial Intelligence (AI) technology advancements have impacted many industries, most notably finance and banking. However, with the development of AI comes a problem: AI is making financial fraud harder to spot.

The repercussions of AI-driven fraud extend beyond the immediate monetary losses. There are substantial costs related to reputation, customer trust, and regulatory compliance. Trust-based business relationships can be eroded due to these fraud incidents, leading to indirect losses that result in direct financial losses.

Traditionally, fraud has been fought using standard detection systems and manual fraud analysis. However, traditional approaches to combat fraud must be revised as fraudsters become more sophisticated,...

more

8 Financial Wellness Metrics for Pre-Retirees

Jeff Martin, CRPC®, Financial Advisor in Arizona

As one approaches retirement, monitoring your financial situation by understanding your net worth and assessing the assets and resources needed to maintain a comfortable lifestyle throughout retirement is vital. This article explores eight key financial wellness metrics that pre-retirees must monitor as they approach retirement.

1. Income replacement ratio. One of the primary financial wellness metrics is the Income Replacement Ratio (IRR), which calculates the percentage of your pre-retirement income that your retirement income will replace. Many individuals work toward a target ratio between 70-80%. Therefore, if you currently make $100,000 annually, your retirement income should ideally be between $70,000 to $80,000.

2. Net worth. Net...

more

A Tax Planning Guide for Retirees

Jeff Martin, CRPC®, Financial Advisor in Arizona

Tax planning is an essential aspect of financial management, especially for individuals who have accumulated substantial wealth over their lifetime. Retirees, in particular, need to pay special attention to their tax planning strategies to help ensure they can address their retirement income and leave a significant legacy for their descendants.

The substantial assets of many retirees often mean they bear a heavier tax burden than others. The key to reducing this tax liability lies in creating a strategic tax plan, utilizing various tax-efficient tools, and remaining agile in response to changes in tax laws. In addition, retirees may consider optimizing tax planning strategies, which include Roth conversions, tax-efficient investments, estate planning, trusts, and charitable...

more

Working a Side Hustle: Benefits and Challenges

Jeff Martin, CRPC®, Financial Advisor in Arizona

An increasing number of full-time workers seek to increase their income through working a side hustle, which is employment in addition to a full-time job. In this article, we'll delve into the benefits of this trend, essential tips for juggling multiple jobs, and the thin line between considering it as a hobby or business income.

The benefits of a side hustle

Although a side hustle offers the potential for more income, its benefits extend far beyond. Side hustles enable individuals to explore their interests or passions outside their full-time jobs. Side hustles often amplify a sense of freedom and self-reliance, reducing job-related stress and burnout.

A side hustle can be an excellent way to strengthen or add to a skill set, which...

more

What Planning Can Help You Achieve in the New Year

Jeff Martin, CRPC®, Financial Advisor in Arizona

Wouldn't it be nice to pay fewer income taxes in retirement? A tax-advantaged strategy called a Roth IRA conversion may lower your taxable income later in retirement. A Roth IRA conversion involves repositioning a traditional IRA or qualified employer-sponsored retirement plan assets into a Roth IRA. There are a few Regardless of your goals, planning at the beginning of the New Year can prepare you to work toward achieving them. One of the most significant benefits of planning is that it gives you the confidence to stay on track toward your goals or make changes to pursue them throughout the year.

To get started, examine your current financial situation by assessing your budget, debt management, savings, retirement savings, and insurance. Next, work toward more complex areas,...

more

Ways to Ensure Generational Wealth Transfers Smoothly

Jeff Martin, CRPC®, Financial Advisor in Arizona

Asset management coupled with financial wellness are crucial for ensuring long-term confidence when wealth transferring from generation to generation. Understanding and implementing appropriate wealth transfer techniques is essential for effectively sharing wealth with the next generations. Here are some essential techniques to help manage generational wealth transfer more confidently:

Participating in Estate Planning- One pillar for managing generational wealth transfer is thorough estate planning. Estate planning doesn't just involve drafting a will; an estate plan should include provisions for the possible incapacity of the wealth owner, power of attorney, healthcare directives, and other appropriate documents for efficient wealth transfer. For families, it's...

more

4 Tips for Capital Gains Tax Planning

Jeff Martin, CRPC®, Financial Advisor in Arizona

As the end of the year approaches, investors need to focus on tax-related considerations, particularly regarding capital gains. Year-end tax planning can help investors manage their overall tax liability while seeking to manage investments for suitable tax outcomes. Here we explore four key tax planning tips for capital gains: what it is, tax law changes, tax-efficiency, and offsetting capital losses.

Tip #1- Understanding capital gains

First, having a good understanding of the concept of capital gains is crucial. In simple terms, a capital gain is the increase in value of an investment or real estate beyond its purchase price. However, this gain is unrealized until the investment sells. The resulting profit from a sale is taxed at a rate...

more

How Recessions Hinder More Than Just Economic Growth

Jeff Martin, CRPC®, Financial Advisor in Arizona

Recessions, defined by consecutive quarters of negative economic growth, have been a cyclical feature of market economies since their inception. While it's tempting to quantify a recession solely in terms of GDP contraction, it's crucial to understand that the implications stretch far beyond economic growth. To truly appreciate the encompassing impacts of a recession, one must delve into various areas that may be affected:

Sociopolitical Considerations- Recessions leave a significant footprint on the socioeconomic landscape of affected nations. In severe cases, recessions may escalate social unrest. Dwindling financial resources can bring heightened competition and intensify socioeconomic issues and political instability. For instance, during the 2008 financial...

more

Social Security Retirement: Changes for 2024

Jeff Martin, CRPC®, Financial Advisor in Arizona

As the landscape of our economy shifts and evolves, so do the policies and practices that guide our federal programs. One such program that undergoes continual alterations and modifications is Social Security. In this article, we will explore the social security changes anticipated in 2024 that could significantly affect Americans who rely on this vital government program.

While the Social Security program, designed to support elderly and disabled citizens, has been a cornerstone of public policy since its inception in 1935, it is not immune to transformations. Social Security Retirement beneficiaries must know these changes to help plan their finances accordingly.

One of the critical changes forecasted is the increase in the Full Retirement Age (FRA). FRA is when people...

more

5 Tax Benefits of Donor Advised Funds

Jeff Martin, CRPC®, Financial Advisor in Arizona

A donor-advised fund (DAF) is a charitable giving vehicle administered by a public charity created to manage charitable donations on behalf of organizations, families, or individuals. The benefits of DAFs extend beyond their primary purpose of facilitating philanthropic activities. One of the main incentives of DAFs is the tax benefits donors receive from giving. Donors can bolster their philanthropic impact by understanding and leveraging these tax advantages:

1. Immediate Charitable Tax Deductions- One tax benefit of DAFs is the immediate charitable tax deduction. When a contribution is made to a DAF, the donor receives an immediate tax deduction in that tax year. The donor can immediately benefit from the tax deduction before the funds are granted to specific...

more

A Year-end Financial Checklist for Investors

Jeff Martin, CRPC®, Financial Advisor in Arizona

Investors must perform a thorough year-end financial review as the year draws close. Whether you're a seasoned investor or a beginner testing the waters of wealth creation, a comprehensive financial evaluation allows you to modify your strategy, rebalance your portfolio, and manage your returns. Below is an eight step year-end financial checklist to help ensure you're on track for financial independence in the New Year.

Step #1- Evaluate your financial goals. The first item on your financial checklist should be taking stock of where you stand with your financial goals. This evaluation may provide a clear insight into how your investments have performed throughout the year and whether or not you've achieved your objectives. It's crucial to assess if these goals...

more

Innovative Ideas for Charitable Giving

Jeff Martin, CRPC®, Financial Advisor in Arizona

Many people are aware of their capacity to impact the world to make it a better place through giving. Philanthropy and charitable giving provide a platform for them to affect positive change beyond wealth accumulation. Charitable endeavors can be personally rewarding while positively impacting the broader society that benefits from their generosity.

The traditional one-time donation is always honorable, but other innovative strategies may have a broader impact. Here are some charitable giving ideas to consider:

Implementing a Donor-Advised Fund (DAF). A Donor-Advised Fund is a philanthropic vehicle that provides an immediate tax benefit to the donor. You contribute financially to the fund and get the privilege to recommend grants to non-profits of your...

more

7 'Tax-Smart' Retirement Withdrawal Strategies

Jeff Martin, CRPC®, Financial Advisor in Arizona

For many, retirement is the phase of life to kick back, relax, and enjoy the fruits of years of working and saving. However, financial decisions before and during retirement can significantly influence our quality of life and tax liability. Therefore, employing tax-smart retirement withdrawal strategies may help you maximize your retirement nest egg.

Here are seven tax-smart retirement withdrawal strategies to help mitigate your tax burden and help you maintain financial confidence throughout retirement:

1. Tap into your non-retirement accounts first. Withdrawing money from your non-retirement accounts may make sense earlier in retirement. Why? The IRS doesn't tax the principal balance you contributed to these accounts. You will only have to pay taxes on...

more

What to Know About Roth IRA Conversions

Jeff Martin, CRPC®, Financial Advisor in Arizona

Wouldn't it be nice to pay fewer income taxes in retirement? A tax-advantaged strategy called a Roth IRA conversion may lower your taxable income later in retirement. A Roth IRA conversion involves repositioning a traditional IRA or qualified employer-sponsored retirement plan assets into a Roth IRA. There are a few reasons why investors may pursue a Roth IRA conversion strategy:

· A Roth provides the flexibility to withdraw money when needed.

· There is no Required Minimum Distribution (RMD).

· A Roth IRA conversion as part of estate planning may help lessen the impact of estate taxes on an estate.

Before initiating a Roth IRA conversation strategy, here are things to consider before making your decision:

...

more

4 Ways to Prepare Now for 2024's Tax Season

Jeff Martin, CRPC®, Financial Advisor in Arizona

The financial decisions you make between now and the end of the year can significantly impact how much you may pay once tax day arrives. If you take action before December 31st, you may reduce your tax burden and keep more of your hard-earned money. Here are some smart tax-saving strategies to consider:

1. Max out your retirement savings contributions- Tax-advantaged retirement accounts such as 401(K)s and IRAs fund with pre-tax dollars. Any additional contributions you make now can help lower your 2023 taxable income. Therefore, max out your retirement account contributions if you before the end of the year. If you receive an end-of-year bonus from your employer, request to contribute it to your pre-tax retirement savings account.

Use the...

more

3rd Quarter End of Year Financial Checklist

Jeff Martin, CRPC®, Financial Advisor in Arizona

As the end of the year approaches, taking time for an end-of-the-year financial check-up is critical. It involves a comprehensive review of your financial position. Assessment can help you understand how you spent your money throughout the year and guide you to make better financial decisions in the forthcoming year. Prepare by using this checklist as you work toward your financial objectives.

1. Review your budget. By revisiting your budget, you can compare and contrast your actual spending with the past budget entries for the year. Reviewing is a great way to help you understand where your money went, gauge if your spending habits have been healthy or not, and decide the areas where you need to cut back. Your budget can also provide insight into investing more...

more

Advancing Women's Health: Sustainable Finance

Jeff Martin, CRPC®, Financial Advisor in Arizona

One challenge Sustainable Finance aims to solve is the advancement of women's health. Sustainable finance and women's health have profound implications in fostering global health equity, empowering women, and advancing socio-economic development. It's important to understand the connection between sustainable finance and women's health;

· Sustainable finance is any form of financial service that integrates environmental, social, and governance (ESG) criteria into its business or investment decisions. Its underlying objective is to promote long-term environmental sustainability and social welfare.

· Women's health encompasses various issues, from reproductive health to non-communicable diseases such as cancer and...

more

Wealth Management For High-Earning Women

Jeff Martin, CRPC®, Financial Advisor in Arizona

In the U.S., women control a third of household assets. But by 2030, U.S. women are expected to control much of the assets that the baby boomer generation will pass to heirs, roughly 30 trillion in assets. High-earning women have become the newest face of wealth and will increase their net worth even more.

High-earning women are becoming the primary ‘breadwinners’ in many families and are increasingly the financial decision-makers. Women have unique needs that often differ from their male counterparts:

· Women have an additional life expectancy of 5 years longer than men.

· Women earn seventy-nine cents to every dollar a man earns.

· Women often take time off from work to care for other family members.

· Women, on average,...

more

Social Security COLA May Be Less in 2024

Jeff Martin, CRPC®, Financial Advisor in Arizona

For 2023, Social Security Retirement and Supplemental Security Income (SSI) benefits increased due to inflation. The increase was 8.7%, resulting in an average monthly benefit increase of $146 per month for a yearly increase of $1,827 in 2023.

Social Security benefits are adjusted yearly for inflation as a cost-of-living adjustment (COLA) based on the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). The CPI-W index measures the monthly price change in a market basket of goods and services, including food, energy, and medical care.

With the inflationary prices Americans experienced in 2022, the 2023 Social Security COLA adjustment helped increase monthly benefits. While we can’t predict what inflation will do in 2023, the Consumer Price Index may...

more

How to Integrate a Gender Lens in Your Investing

Jeff Martin, CRPC®, Financial Advisor in Arizona

Gender lens investing is a type of impact investing that aims to create a beneficial social or environmental impact and an expected financial return. What differentiates gender lens investing is that it is an investment that, from its inception, is intended to benefit women and girls.

Gender lens investing considers gender-based factors in investment decision-making to advance gender equality. Gender lens investing may benefit women and girls in two distinct ways:

#1- Investing with the intent to address gender issues or promote gender equality by:

- Investing in women-owned or women-led enterprises

- Investing in enterprises that promote workplace equity (in staffing, management, boardroom representation, and along their supply chains);...

Asset Location Strategies Using Taxable, Tax-Deferred, and Tax-Exempt Accounts

Jeff Martin, CRPC®, Financial Advisor in Arizona

Understanding the difference between taxable, tax-deferred, and tax-exempt accounts may improve portfolio diversification and how much return you earn over time. But often, investors may not fully understand how a strategy called asset location may help improve returns and lower their overall tax bill using these different types of accounts. Each account type has different tax rules and treatments, and understanding each may help you determine which accounts suit your situation. Here, we outline what you need to know about each account type:

Taxable accounts- A taxable account is an account for which the IRS default rules apply, meaning there are no tax benefits. However, taxable accounts often have fewer restrictions and more flexibility when investing and...

more

Why Starting a Business After a Career Setback Will Bring You Back to Life

Jeff Martin, CRPC®, Financial Advisor, Arizona

Without a doubt, losing your job or being laid off can be an incredibly difficult experience. But it can also be an opportunity to start fresh and take control of your career. Starting your own business is one way to do this. Here are some reasons why you might want to consider starting your own business after a career setback, courtesy of J. Martin Wealth Management.

Become the Boss

When you start your own business, you become the boss. You have the freedom to make decisions about how you want to run things and what direction you want to take the company in....

more

Annuities: What They Are and How They Work

Jeff Martin, CRPC®, Financial Advisor in Arizona

Having enough retirement income is a top concern for many Americans nearing or in retirement. Even though they may have saved consistently throughout the working years, they may be concerned that their retirement plans will succeed. A successful retirement plan provides the ability to maintain your lifestyle for the duration of your life.

Having enough retirement income for what you need and want is essential and must be planned for, even in the best economic conditions. A way to provide income safety is by using annuities as an asset class in your retirement portfolio.

Annuities Provide Safety and Income- Annuities help retirees address a specific retirement planning risk- Longevity Risk. Longevity Risk is the risk that a retiree outlives their financial...

more

What You Need to Know About Purchasing Life Insurance

Jeff Martin, CRPC®, Financial Advisor in Arizona

Life insurance is a great addition to your portfolio that help can protect your loved ones and beneficiaries if you unexpectedly pass away. While no amount of money can ease the grief of losing someone, life insurance may help reduce the financial burden they may face. It's important to know how life insurance works and what to consider when purchasing life insurance so you can make an informed decision before you buy.

What Does Life Insurance Cover?

Life insurance can be used to help your beneficiaries pay for your funeral costs and a variety of other expenses, including:

- Everyday bills

- Wage loss

- Child care

- Debts

- College tuition

- Business debts

It’s important to note that life...

more

3 Ways to Save for Your Child's Retirement

Jeff Martin, CRPC®, Financial Advisor in Arizona

Helping your child save for retirement starts with financial education and discussing the importance of saving for their future. Besides financial education, there are strategies to help them get a head start their retirement savings. Here are three ways to start saving for your child's retirement now:

#1 Life Insurance- Whole life insurance, also called cash-value life insurance, doesn’t expire, meaning your child can’t outlive it. Whole life insurance features a death benefit and a cash value, which accrues interest at a fixed rate. If one continues to pay the premiums, your child can tap into the cash value by taking a policy loan or a cash withdrawal later to help fund retirement. Here are some reasons why investing in a life insurance policy for your child...

more

6 Tips For Saving on Summer Travel

Jeff Martin, CRPC®, Financial Advisor in Arizona

If you love to travel, summer is a great time to do so and have new experiences near home or far away. As you plan, remember to budget for travel expenses and look for ways to save during the peak summer travel season. Here are some tips to help you save on summer travel:

#1- Create a travel bucket list. You may want to travel to a few different places this summer. Create your travel itinerary with the understanding that plans may change and be flexible. Remember to leave time in your itinerary to rest, relax, and disconnect- and not spend money. Enjoy the sunrise, sunset, parks, and places that are free too!

#2- Do your research. Once you decide where you want to travel, create an estimated budget. Conduct your...

more

Achieving Financial Wellness: How to Change Your Money Mindset

Jeff Martin, CRPC®, Financial Advisor in Arizona

Achieving financial wellness can seem like an impossible task. It's easy to be overwhelmed by the intricacies of personal finance, but with the right money mindset, you can be successful. By following these simple tips, you can start to make positive changes in your financial outlook.

The Benefits of Prioritizing Long-Term Goals

It's easy to get caught up in short-term desires for things that aren't necessary for long-term success or stability. When it comes to managing your finances, make sure you prioritize long-term goals over instant gratification. This means...

more

Unused 529 Plan Funds? You Have Spending Options

Jeff Martin, CRPC®, Financial Advisor

529 plans are tax-advantaged savings vehicles designed to accumulate contributions and help pay for the beneficiary's qualifying education expenses. Sometimes, 529 plans have unused funds after the beneficiary graduates or decides to discontinue their education. Whatever the reason for having unused 529 plan funds, you have options of what you can do with the monies. Here are five options to consider:

more

Long-Term Care Tax: New Legislation That May Impact You

Jeff Martin, CRPC®, Financial Advisor

As our population ages, discussions about long-term care (LTC) and who pays for it are essential for many families and state governments. LTC is ongoing care in a care facility, nursing home, or at home for those unable to perform a certain number of activities of daily living (ADL) without assistance. ADLs include eating, bathing, dressing, toileting, transferring in and out of bed, continence, or when physical, mental, or cognitive function is impaired, or when a doctor has ordered specific care.

For those with LTC insurance (LTCI), ADLs determine when the policy will start paying for their care. Paying for LTC can be costly until the policy begins to pay after a set time, such as 60 or 90 days. During that time, it is up to the individual to pay depending on their level of...

more

529 Plans: For Education and Transferring Wealth

Jeff Martin, CRPC®, Financial Advisor

529 plans can help build generational "education" wealth since the plan can pass down from one beneficiary to a beneficiary of the next generation. Here are three 529 plan wealth transfer tax saving strategies to consider:

more

Bank and Brokerage Firm Failures: What FDIC Insurance and SIPC Covers

Jeff Martin, CRPC®, Financial Advisor

For bank customers and investors, the news may have left them wondering what they would do if this was their financial institution. Bank customers and investors have some protection through FDIC insurance or SIPC, but understanding what each cover can help them plan for failure risk.

moreStrengthen Your Small Arizona Business with a Safety Net

Jeff Martin, CRPC®, Financial Advisor

Every small business needs a safety net. A safety net is a buffer that can help you weather the storms of running a business. It can take many forms but typically includes cash reserves, lines of credit, and insurance. In this blog post, financial advisor Jeff Martin explores how to create a safety net for your small Arizona business.

Increase Your Cash Reserves

One of the most important parts of a safety net is cash reserves. These are funds that you set aside specifically for tough times. That way, when unexpected expenses arise or revenue dips, you have the money on hand to cover them. We recommend setting aside enough cash to...

more

529 Plan: Who Should Consider Opening One and Who Can Set Them Up?

Jeff Martin, CRPC®, Financial Advisor

Who should have a 529?

A 529 plan is a tax-advantaged savings plan designed to help families save for education expenses. It can be used to save for qualified expenses at any eligible educational institution, including colleges, universities, and vocational schools. Here are some guidelines on who should consider opening a 529 plan:

Parents and grandparents: Parents and grandparents who want to save for a child's education should consider a 529 plan. By starting early and contributing regularly, they can help to ensure that the child has the financial resources necessary to pursue their education goals.

High-income earners: High-income earners may benefit from the tax advantages of a 529 plan. Contributions to a 529 plan are made with after-tax dollars, but earnings...

moreSmart Strategies for Increasing Your Net Worth at Every Stage of Life

Jeff Martin, CRPC®, Financial Advisor

The key to increasing net worth throughout different stages of life is to start early and be consistent. In the 20s, financial goals should be set to prioritize spending, reduce debt, and start saving early. Investing in education, increasing income, and living below means can also contribute to net worth growth. In the 30s, investment in a diversified portfolio and saving for retirement, buying a home, and increasing income are some ways to increase net worth. In the 40s, increasing retirement savings, paying off high-interest debt, and investing in real estate are recommended. As you approach retirement in your 50s, it's important to maximize retirement account contributions, diversify investments, re-evaluate insurance needs, and reduce debt. Rental property investments and...

more

Leaving Your Employer? You Have Options For Your 401(k)

Jeff Martin, CRPC®, Financial Advisor

You may assume that you must rollover your 401(k) when leaving your employer into another retirement savings plan. However, depending on the 401(k) plan document and if a rollover is appropriate for your situation, it may be optional.

more

Springtime Is Clean Your Finances Time

Jeff Martin, CPPC®, Financial Advisor

Springtime is a great time to review your finances so you can work toward financial independence. While many are organizing their closets and cleaning out drawers and garages, instead, clean up your finances using these ten tips:

more

Five Signs That Indicate Interest Rates May Rise

Jeff Martin, CRPC®, Financial Advisor

The Social Security Trust Fund’s Problem

Jeff Martin, CRPC®, Financial Advisor

Social Security (SS) taxes and other income are deposited into the trust fund accounts, and SS benefits payout from them. The only purpose for which these trust funds are used is to pay benefits and program administrative costs.

more

SECURE ACT 2.0 HIGHLIGHTS

Jeff Martin

The SECURE 2.0 and RILA Acts were signed into law on December 29, 2022 as part of the FY23 Omnibus Appropriations Act, signed by President Biden. The SECURE 2.0 Act has 92 provisions and affects most employers and employees participating in workplace retirement plans. Clarifications are expected from regulatory agencies in the coming months.

Some of the 2023 provisions include:

- The required minimum distribution age will be raised to 73 (effective January 1, 2023) and 75 (effective January 1, 2033).

- The individual tax penalty for failing to take the required minimum distribution will be reduced to 25% (possibly 10% if corrected within 2 years).

- The limit for purchasing qualified longevity annuity contracts is increased to $200,000 (adjustable for...

10 TIPS TO DEVELOP FINANCIAL WELLNESS THIS YEAR

Financial wellness is essential for many reasons since it can impact your mental and physical health and overall quality of life. By improving your financial wellness, you can build wealth for a more financially secure future.

more

HOW BEHAVIORAL ECONOMICS CAN HELP YOU KEEP NEW YEAR'S FINANCIAL RESOLUTIONS

Financial wellness is essential for many reasons since it can impact your mental and physical health and overall quality of life. By improving your financial wellness, you can build wealth for a more financially secure future.

more

INDEPENDENT AND THRIVING: WHAT TO CONSIDER IN YOUR LATER YEARS

If you're still working and nearing retirement, planning the subsequent decades of your life is crucial. It starts with a healthy mindset, body, and financial wellness.

more

5 VALENTINE'S DAY GIFTS YOUR PARTNER WILL LOVE

As your financial advisor, I can help you determine which gift is appropriate for your partner and strives to most likely leave a dynamic impression that lasts throughout this year and beyond.

more

TAX SAVING MOVES TO MAKE BEFORE 2022 ENDS

You can take action to help lower your 2022 tax bill later. It would help if you made contributions, or distributions, so you don't miss out on these tax-saving strategies. Here are five tax-saving moves to make now to help lower your taxable income:

more

A DIVORCE PLANNING FINANCIAL CHECKLIST

Marriages can end for many reasons; infidelity, stress, personality changes, and finances. Divorce can be difficult for children and extended family and devastating to your finances and assets that you've accumulated together. Couples participate in financial planning, personal budgets, and savings and spending plans when marriages are going well. It is vital to continue financial planning for yourself now while starting the divorce process and after your marriage ends.

more

SURVIVAL TIPS FOR TOUGH ECONOMIC TIMES

During an economic slowdown, times can be challenging for many, often leading to layoffs, inflation, and rising interest rates. Economists suggest that the U.S. economy is not in the clear and may be approaching another recession in 2023, according to an Associated Press article. Knowing the signs of a recession is essential to help you determine when to cut spending. You can also look for extra cash by using these tips to help you survive tough economic times:

more

SOCIAL SECURITY COLA AND MEDICARE: WHAT YOU NEED TO KNOW FOR 2023

Social Security Retirement and Supplemental Security Income (SSI) benefits will increase by 8.7 percent in 2023, the most significant increase since the 1980s. The last time the cost-of-living adjustment was higher was in 1981 when the increase was 11.2%. The increase, due to inflation, will result in a Social Security benefits increase of an extra $146 per month, or $1,827 for 2023, up from $1,681 in 2022.

more

SOCIAL SECURITY RETIREMENT BENEFITS: MILESTONE AGES THAT IMPACT YOUR PAYOUT

Understanding the critical ages for taking Social Security retirement benefits can be the difference in thousands of dollars over time. Therefore, it is important for you to determine the best age to start taking Social Security for your situation. Here are the important ages on the Social Security retirement benefits timeline to consider that may impact your monthly payout:

more

A MONTHLY CHECKLIST TO HELP YOUR BUILD FINANCIAL SECURITY

If it seem overwhelming to keep you finances on track and implement multiple financial actions at once, a month-by-month approach may help. Tackling financial tasks helps ensure you're working towards reaching your financial goals and checking tasks off of your to-do list each month. While some financial tasks are time-sensitive, others can be completed throughout the year. Here is a month-by-month checklist list to help keep your finances on track throughout the year:

more